Ten popular car taillights

At present, the gap between domestic and international automotive lighting technology is mainly reflected in the high-end car light products. In the field of LED lights, the development of domestic low-power LED applications is relatively mature. According to China's LED online estimates, the current penetration rate of the interior lights and rear lights is close to the international level, and the daytime running light LED penetration rate has reached 47%. .

The development of medium and high power LED applications has been slow, and the high-power far-and-far light and fog light products are still dominated by international manufacturers because of the high technical threshold. Therefore, the penetration rate is still very low. In recent years, domestic autonomous lamp companies have made considerable technological progress.

Changzhou Xingyu, the leader of domestic car lights, has entered the global market supporting system for the support of high-end luxury cars such as BMW and Mercedes-Benz. In 2014, the company obtained the Audi SUV rear combination lamp development project, passed the review of German BMW supplier, and successively obtained the side turn signal and charging indicator development project.

In addition, Xingyu began to enter the field of smart headlights. In 2014, the company's first AFS headlamp was successfully developed and put into operation. Currently, it is mainly equipped with GAC Group's autonomous SUVs.

Chinese domestic company Snowlight Optoelectronics has relatively technical advantages in the field of xenon lamps, and is the only manufacturer in the global automotive xenon lamp industry with the exception of Philips, which owns the intellectual property system.

Snowlight is the world's third and only Asian vehicle lighting company that has passed comprehensive vehicle testing and certification. It cooperates with Chery, JAC, Huatai, Geely, Brilliance, Changan and other automobile manufacturers to provide HID vehicle xenon lamp vehicle support.

In order to break through the technical blockade of foreign manufacturers, domestic automotive lighting and automotive lamp assembly manufacturers have increased investment, especially in the field of LED lights gradually compensate for the gap between domestic and foreign, to speed up the process of localization of car lights.

We found that in the R&D center setup, supply chain, and factory layout, leading automotive lighting companies increasingly began to localize their layout, thereby reducing costs and competing for market share. In the domestic market, the trend of localized production of the automotive lamp industry and the rise of independent brands is very clear. Specifically, we believe that the driving factors include:

The rise of joint-venture vehicle manufacturing companies' purchase localization and self-owned brand vehicle manufacturing companies, the products of self-owned brand automotive lighting manufacturers have a cost-effective advantage. In order to cope with increasing market competition and reduce procurement costs, the original joint-venture vehicle manufacturers that originally only purchased products from foreign automotive lighting brands began to reform the component supply system, and the range of procurement targets gradually expanded to leading domestic suppliers.

The local vehicle manufacturing companies are major customers of domestic-funded automotive lighting manufacturers. Along with the development and expansion of Chery Automobile, Geely, BYD, and other independent branded companies, the share of local vehicle manufacturers in the passenger vehicle market has gradually expanded, making domestic-owned automotive lamps. The development of enterprises provides good opportunities.

Technological advances have overturned the inherent competitive landscape. Local companies have accelerated their layout to achieve a curve overtaking, and product technology in the automotive lighting sector has been replaced faster. This includes the integration of new lighting technologies such as laser and OLED technologies, and the development of new lighting systems, namely advanced headlight systems; Integration of new components, including cameras and sensors (for advanced headlight systems); development of new knowledge and capabilities, such as image processing technology (for advanced headlight systems).

New technologies or functions will make the relationship between vehicle manufacturers and device or component developers (ie, secondary and tertiary suppliers) and new suppliers become closer, resulting in more and more vehicle manufacturers bypassing one another. Level suppliers, thus creating new supply chains and value chains.

OEMs' laser lighting applications and optical engineering development can directly cooperate with secondary or tertiary suppliers, which enables them to fully control the development and mastery of related technologies. As a result, technological changes have provided opportunities for the up-and-coming local lighting companies to turn corner cars.

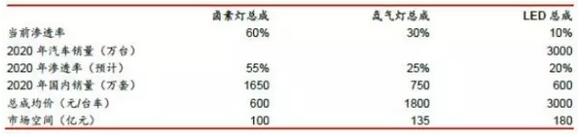

The current mainstream products in the automotive market are halogen lamps and xenon lamps. The LED penetration rate is relatively low. Halogen lamps are mainly installed in mid- to low-end models, while xenon lamps are assembled in high-end models. LEDs are mainly used in high-end models because of their higher cost.

With the development of automotive lighting technology in the direction of energy saving, lightweight, and electronic, we judge that the LED penetration rate will gradually increase, and the halogen lamp will decline relatively. Assuming that China will sell 30 million vehicles in the 2020 market, we expect the market for halogen lamps, xenon lamps, and LED assemblies to reach 100/135/18 billion yuan respectively.